Medicare Prescription Drug Plans: A Complete Guide

Millions of Americans depend on Medicare prescription drug plans to help pay for their medications. If you’re approaching age 65, already on Medicare, or just want to understand your options, this guide will help you make confident decisions. We’ll break down how these plans work, what they cover, and how to choose the right plan for your needs—using clear, simple language.

What Are Medicare Prescription Drug Plans?

Medicare prescription drug plans are known as Part D. They are insurance plans that help pay for prescription drugs for people who have Medicare. You can get Part D in two ways:

- Standalone Part D plans: These work with Original Medicare (Parts A and B).

- Medicare Advantage plans (Part C): Some Advantage plans include drug coverage.

You pay a monthly premium for Part D, plus some costs when you fill prescriptions. These plans are offered by private insurance companies, not by Medicare itself. Each plan can cover different drugs and have its own costs.

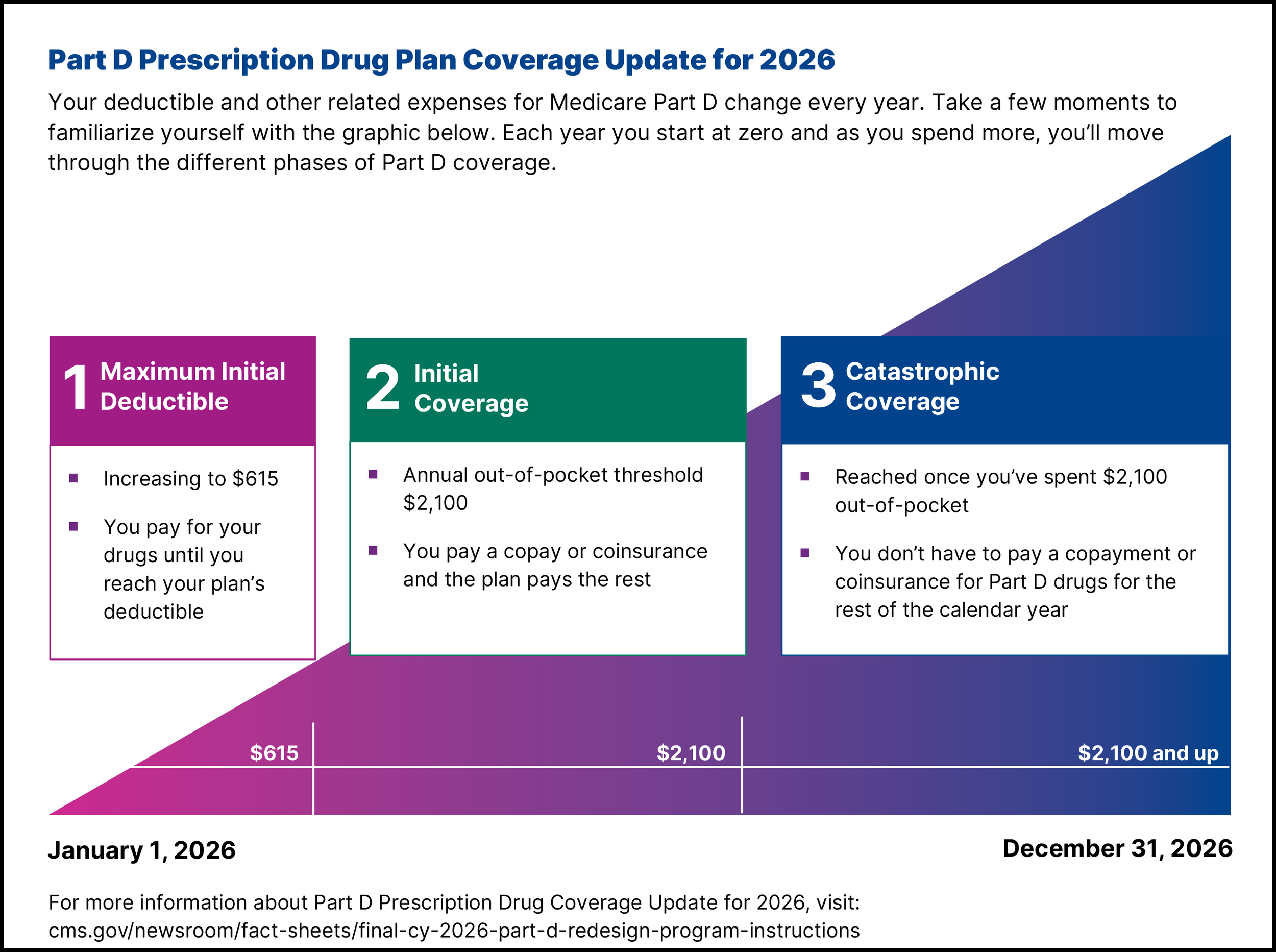

How Do Medicare Part D Plans Work?

Part D plans help cover the cost of drugs at your local pharmacy. Here’s how the process generally works:

- You enroll in a Part D plan.

- You pay a monthly premium (average $34.70 in 2024).

- When you buy medicine, you pay a share of the cost. This could be a copay (fixed amount) or coinsurance (percentage).

- Each plan has a formulary—a list of drugs it covers.

- Plans have pharmacy networks. You usually pay less at certain pharmacies.

Most plans split drug costs into stages. Here’s a simple breakdown:

| Stage | What You Pay | 2024 Example |

|---|---|---|

| Deductible | You pay all drug costs until deductible is met | Up to $545 |

| Initial Coverage | Plan pays, you pay copay/coinsurance | Until total drug costs reach $5,030 |

| Coverage Gap (“Donut Hole”) | You pay higher share | 25% of drug cost |

| Catastrophic Coverage | Plan pays most costs | Small copay or coinsurance |

Many people worry about the donut hole (coverage gap), but recent changes have made it less costly. You pay 25% for both brand-name and generic drugs during this period.

What Do Part D Plans Cover?

Every Part D plan must cover a wide range of drugs, but not all plans cover the exact same medications. Here’s what you can expect:

- All plans must cover drugs in key categories (like cancer, HIV/AIDS, antidepressants).

- Each plan has a formulary. Check if your medicines are included.

- Some drugs may need prior authorization (approval before coverage).

- Plans may have quantity limits or require you to try cheaper drugs first (step therapy).

If your medicine isn’t on the formulary, you can request an exception. Still, not all exceptions are approved.

Who Is Eligible For Medicare Prescription Drug Plans?

To sign up for a Part D plan:

- You must have Medicare Part A and/or Part B.

- You must live in the plan’s service area.

- You cannot have both a standalone Part D and a Medicare Advantage plan with drug coverage.

Enrollment periods matter. The best time is when you first become eligible for Medicare—known as the Initial Enrollment Period. If you miss it, you may have to wait until the Annual Enrollment Period (October 15–December 7).

How Much Do Medicare Drug Plans Cost?

Costs vary by plan, location, and your chosen drugs. Here are the main costs:

- Monthly premium: Average $34.70, but can be higher or lower.

- Annual deductible: Up to $545 in 2024.

- Copay/coinsurance: Depends on the drug tier.

- Extra premium for high-income earners (Income Related Monthly Adjustment Amount).

Let’s compare sample plans:

| Plan Name | Monthly Premium | Annual Deductible | Preferred Generic Copay |

|---|---|---|---|

| Plan A | $32 | $545 | $5 |

| Plan B | $38 | $0 | $10 |

| Plan C | $29 | $400 | $7 |

Notice that a lower premium can mean a higher deductible or copay. Always check the details.

How To Choose The Right Medicare Prescription Drug Plan

Picking the best plan for you means looking at more than just the premium. Here’s how to make a smart choice:

- List your current medicines. Check if they’re covered.

- Compare costs. Look at premium, deductible, copays, and coinsurance.

- Check pharmacy network. Are your favorite pharmacies included?

- Review the formulary. Each plan’s list of covered drugs is different.

- Look for extra benefits. Some plans offer mail-order or home delivery.

- Consider star ratings. Medicare rates plans from 1–5 stars for quality.

- Estimate your yearly cost. Use Medicare’s Plan Finder tool.

Many beginners focus only on premiums, but total yearly cost is more important. Also, switching plans is possible every year during open enrollment.

Drug Tiers And How They Affect Your Costs

Most Part D plans group drugs into tiers. Higher tiers cost more. Here’s a typical structure:

| Tier | Drug Type | Sample Copay |

|---|---|---|

| 1 | Preferred Generics | $5 |

| 2 | Other Generics | $10 |

| 3 | Preferred Brands | $35 |

| 4 | Non-Preferred Drugs | $80 |

| 5 | Specialty Drugs | 20% coinsurance |

Always check which tier your medicine falls into, as this changes the price you pay.

Common Mistakes When Choosing A Plan

Many people make mistakes that can cost them money or limit their choices:

- Ignoring the formulary: Not checking if your drugs are covered.

- Assuming all pharmacies are in-network: Using a pharmacy outside the network raises costs.

- Missing enrollment deadlines: Can lead to late enrollment penalties.

- Choosing lowest premium blindly: May pay more overall if copays/deductibles are high.

- Not reviewing changes each year: Formularies and costs can change annually.

A smart approach is to review your plan every fall, even if you’re happy with it.

Financial Help: Extra Help Program

If you have limited income and resources, you may qualify for Extra Help. This program covers most drug costs and lowers premiums, deductibles, and copays. In 2024, people with income below $22,000 (individual) or $29,000 (couple) may qualify. Apply through Social Security or your state’s Medicaid office.

Practical Examples And Insights

Let’s look at two real scenarios:

- Maria takes three medicines. Her preferred plan covers two but not the third. She checks another plan, finds all three covered, and saves $450 per year.

- John uses a pharmacy outside his plan’s network. He pays double the usual copay. After switching to a preferred pharmacy, his costs drop by 40%.

Beginners often overlook the importance of the pharmacy network. Also, some plans offer mail-order, which can save time and money.

How To Enroll In A Medicare Prescription Drug Plan

Follow these steps:

- Create a list of your medicines.

- Visit the Medicare Plan Finder at medicare.gov.

- Compare plans by cost, coverage, and pharmacy network.

- Check star ratings for plan quality.

- Enroll online, by phone, or with a local agent.

Enrollment periods:

- Initial Enrollment Period: When you first qualify for Medicare.

- Annual Enrollment Period: October 15–December 7.

- Special Enrollment Period: For certain life changes (moving, losing coverage).

Missing the window can mean paying a late enrollment penalty, which lasts as long as you have Part D.

Key Data And Trends

- Over 51 million Americans had Part D coverage in 2023.

- Average out-of-pocket cost for Part D users: About $500/year.

- Most popular drugs: Cholesterol, blood pressure, diabetes medications.

- 75% of beneficiaries use preferred pharmacy networks.

Plan details change every year. In 2024, many plans have adjusted their drug lists and costs. Always review your plan before renewing.

Non-obvious Insights

- Mail-order pharmacies often offer lower copays and 90-day supplies, but not all plans include them. Check before choosing.

- Tier exceptions: If your drug is in a high-cost tier, you can request a lower tier placement. Many people don’t know this option exists.

Resources For More Information

For official information, visit Medicare.gov. This site offers plan comparison tools, enrollment guides, and updates.

Frequently Asked Questions

What Happens If I Miss The Enrollment Period?

If you miss your Initial Enrollment Period or Annual Enrollment Period, you may have to wait until the next enrollment window. You might also pay a late enrollment penalty—an added premium for each month you were without coverage.

Can I Change My Medicare Prescription Drug Plan Every Year?

Yes, you can switch plans during the Annual Enrollment Period (October 15–December 7). This is the best time to review your current plan and choose a new one if your needs have changed.

Do All Part D Plans Cover The Same Drugs?

No. Each plan has its own formulary—a list of covered drugs. Always check if your medicines are included, as coverage can vary between plans.

Is There Help For People With Low Income?

Yes. The Extra Help program helps pay for drug costs if your income and resources are limited. It covers premiums, deductibles, and copays. Apply through Social Security or your state Medicaid office.

Can I Use Any Pharmacy With My Part D Plan?

Not always. Most plans have a network of preferred pharmacies. Using a pharmacy outside the network can mean higher costs or limited coverage. Always check your plan’s pharmacy list.

Medicare prescription drug plans can feel confusing at first, but understanding your options will help you save money and get the medications you need. Use the tips above, review your plan yearly, and don’t hesitate to ask for help if you need it.

With the right plan, you’ll have peace of mind and good health coverage.

Read More:

- Affordable Health Insurance Quotes: Save Money on Quality Coverage

- Short Term Health Insurance Online: Fast, Flexible Coverage Today

- Compare Family Health Insurance Plans: Find the Best Coverage

- Private Health Insurance UK: Top Benefits and Best Plans Explained

- Best Private Health Insurance Plans: Top Choices for 2024

- Medicare Supplement Plans Comparison: Find the Best Coverage

- Medicare Dental and Vision Coverage: What You Need to Know

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage