Private Health Insurance Uk: A Complete Guide

Healthcare is a top concern for many people in the UK. The National Health Service (NHS) provides free medical care to everyone, funded by taxes. But NHS services can sometimes be crowded, with long waiting times for treatment and specialist appointments. That’s why more people are considering private health insurance—a way to access faster, more flexible healthcare. This article explains everything you need to know about private health insurance in the UK, including how it works, what it covers, how much it costs, and how to choose the best policy for your needs.

What Is Private Health Insurance?

Private health insurance is a contract between you and an insurance company. You pay a monthly or yearly fee (called a premium), and the insurer pays for some or all of your medical costs if you need treatment. You can use private hospitals, clinics, and specialists, often with shorter waiting times and more comfort.

In the UK, private health insurance is optional. Most people use the NHS, but private cover offers extra benefits—especially for non-emergency treatments or elective surgery.

Main Types Of Private Health Insurance

There are two main types:

- Personal health insurance: Cover for individuals or families.

- Company health insurance: Offered by employers to staff, often as part of a benefits package.

You can buy insurance directly from a provider, through a broker, or sometimes through your workplace.

Key Benefits Of Private Health Insurance

Private health insurance offers several advantages over relying only on the NHS:

- Shorter waiting times: Quick access to diagnosis and treatment.

- Choice of hospital: You can pick from a list of private hospitals and clinics.

- Private rooms: More comfort and privacy during your stay.

- Specialist access: You may see specialists who do not work for the NHS.

- Treatment flexibility: Some policies cover treatments not available on the NHS.

Some people buy private health insurance for peace of mind, knowing they can get fast, quality care if needed.

What Does Private Health Insurance Cover?

Coverage depends on the policy. Most basic policies include inpatient treatment (when you stay overnight in hospital) and day-patient treatment (when you don’t stay overnight). More comprehensive plans add extra benefits.

Here’s a typical breakdown:

| Coverage Type | Basic Plan | Comprehensive Plan |

|---|---|---|

| Inpatient care | Yes | Yes |

| Day-patient care | Yes | Yes |

| Outpatient care | No | Yes |

| Specialist consultations | No | Yes |

| Diagnostic tests (MRI, X-ray) | Limited | Yes |

| Physiotherapy | No | Yes |

| Dental/Optical cover | No | Optional |

| Mental health cover | No | Optional |

Many policies exclude chronic conditions, emergency care, pregnancy, and cosmetic surgery. Always read the policy details carefully.

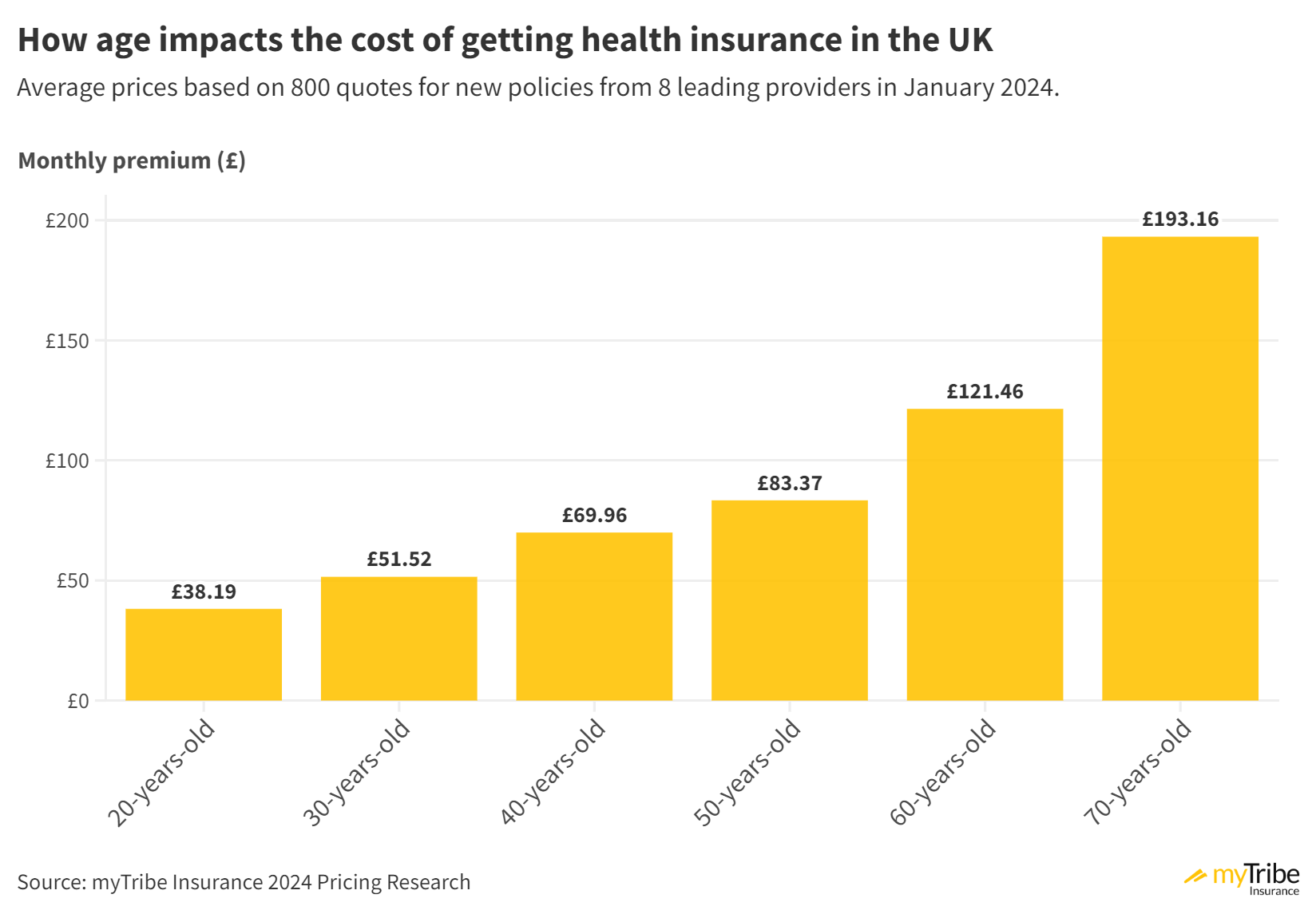

How Much Does Private Health Insurance Cost?

The price of private health insurance varies. Factors affecting your premium include:

- Age: Older people pay more.

- Health: Existing conditions may raise the cost.

- Location: London and some cities are more expensive.

- Coverage level: More benefits mean higher premiums.

- Excess: The amount you pay yourself before insurance covers the rest.

Average costs (2023 data):

- Basic individual policy: £30–£60 per month

- Comprehensive policy: £70–£150 per month

- Family policy: £100–£250 per month

Here’s a quick comparison of average monthly costs for different profiles:

| Profile | Basic Plan (£) | Comprehensive Plan (£) |

|---|---|---|

| Young adult (25) | 35 | 80 |

| Middle-aged (45) | 55 | 120 |

| Family (2 adults, 2 children) | 110 | 220 |

Prices change yearly and between providers. Compare policies to find the best value.

How To Choose The Right Private Health Insurance

Picking the best private health insurance is not just about price. Consider these steps:

- Decide your needs: Do you want inpatient-only, or full outpatient cover?

- Check hospital lists: Does the policy cover hospitals near you?

- Look for extras: Dental, optical, and mental health cover may be important.

- Compare excess amounts: Higher excess means lower premiums, but more out-of-pocket costs.

- Review exclusions: Understand what is not covered.

- Read reviews: Check customer service ratings and claim speed.

- Ask about no-claims discounts: Some insurers reward you for not claiming.

Here’s a comparison table of popular UK providers and their features:

| Provider | Hospital Network | No-Claims Discount | Extras Offered |

|---|---|---|---|

| Bupa | Wide | Yes | Dental, Optical |

| AXA PPP | Wide | Yes | Mental Health |

| Vitality | Medium | Yes | Wellness Rewards |

| Aviva | Medium | No | Child Cover |

| WPA | Selective | Yes | Flexible Options |

Non-obvious insight: Many people forget to check hospital locations on their insurer’s list. If your policy covers only certain hospitals, you may need to travel far for treatment, which can be inconvenient.

What Is Not Covered By Private Health Insurance?

Most UK private health insurance policies have exclusions. These typically include:

- Emergency care: Accidents and emergencies are handled by the NHS.

- Pre-existing conditions: Health problems you had before buying insurance.

- Chronic illnesses: Long-term conditions like diabetes, asthma, heart disease.

- Pregnancy and childbirth: Usually not covered.

- Cosmetic surgery: Non-medically necessary procedures.

Some policies offer partial coverage for these, but most do not. Always check the details before buying.

Non-obvious insight: Even if you have private health insurance, you will still use the NHS for emergencies. Private insurance is mainly for planned treatments and specialist care.

How Claims Work

If you need treatment, follow these steps:

- See your GP: They diagnose and recommend treatment.

- Contact your insurer: Explain your situation and get approval.

- Arrange treatment: The insurer tells you where to go and what is covered.

- Pay any excess: If your policy has an excess, pay this to the provider.

- Insurer pays the rest: They settle the bill directly with the hospital or clinic.

Make sure to keep all paperwork and approval emails. Insurers may reject claims if you do not follow the correct process.

Advantages And Disadvantages Compared To Nhs

Private health insurance is not for everyone. Here are the main pros and cons:

Advantages

- Fast access to treatment and diagnosis.

- Choice of hospital and specialist.

- Comfort with private rooms and facilities.

- Extras such as dental or mental health cover.

Disadvantages

- Costly premiums for long-term cover.

- Exclusions for many health conditions.

- Still need NHS for emergencies and chronic care.

- Complex policies with many details to understand.

Some people find that a basic policy is enough, while others prefer full coverage. Your health, budget, and location will guide your choice.

Who Should Consider Private Health Insurance?

Private health insurance is useful for:

- People who want quick access to treatment.

- Those living in cities with long NHS waiting lists.

- Families seeking more comfort and flexibility.

- Employees whose companies offer insurance as a benefit.

It is less necessary for people who are happy with NHS care and do not mind waiting.

How To Reduce Your Premium

To lower your private health insurance costs:

- Choose a higher excess (you pay more, insurer pays less).

- Select inpatient-only cover (skip outpatient benefits).

- Limit your hospital network to local clinics.

- Use a no-claims discount (if available).

- Pay annually instead of monthly (some providers offer discounts).

- Live a healthy lifestyle—some insurers reward non-smokers and active people.

Compare providers and negotiate for better rates if you have a good health history.

How Private Health Insurance Works With Nhs

Private insurance does not replace the NHS. You can use both. For example:

- Use NHS for emergencies, chronic conditions, and maternity care.

- Use private insurance for elective surgery, specialist consultations, and extra comfort.

Some treatments may start with the NHS and finish privately. You can switch back and forth, but always check if your insurance allows this.

Are Private Hospitals Better Than Nhs?

Private hospitals often provide quieter, more comfortable environments, but NHS hospitals usually have more specialist staff and equipment for emergencies. Private care is best for planned treatments and surgeries, while the NHS is strongest in urgent care.

A good example: hip replacement surgery. NHS patients may wait months, while private insurance can reduce this to weeks. However, the surgery quality and safety are similar—private care mainly offers speed and comfort.

Regulations And Consumer Protection

The Financial Conduct Authority (FCA) regulates private health insurance in the UK. Providers must follow strict rules to protect consumers. If you have problems, you can complain to the Financial Ombudsman Service.

Always check your insurer is FCA registered. For more information about regulation, visit Financial Conduct Authority.

Common Mistakes When Buying Private Health Insurance

Many beginners make errors when choosing a policy:

- Not checking hospital lists—may result in long travel.

- Ignoring excess amounts—could face big bills.

- Missing policy exclusions—find out after it’s too late.

- Forgetting to ask about no-claims discounts.

- Not reading customer reviews—service can vary.

Careful research and asking questions can save money and stress.

Frequently Asked Questions

What Is The Difference Between Private Health Insurance And Nhs?

The NHS is free for everyone and funded by taxes. Private health insurance is paid for by you, and offers faster access, more comfort, and extra services.

Can I Use Private Health Insurance For Emergencies?

No. Emergencies (like accidents or sudden illness) are handled by the NHS. Private insurance covers planned treatments and specialist care.

Does Private Health Insurance Cover Dental And Eye Care?

Some policies include dental and optical cover, but not all. Check the policy details or add these as extras if needed.

How Do I Claim With Private Health Insurance?

Contact your insurer before treatment. Get approval, follow their instructions, and pay any excess. The insurer pays the rest directly to the provider.

Is Private Health Insurance Worth It In The Uk?

It depends on your needs, budget, and location. If you want quick access and extra comfort, it can be worthwhile. For emergencies and chronic care, the NHS remains essential.

Private health insurance in the UK offers flexibility, speed, and added comfort—but it’s not a replacement for the NHS. If you plan carefully, understand your needs, and research providers, you can find a policy that fits your lifestyle and budget.

Remember to check hospital networks, extras, exclusions, and costs before deciding. With the right policy, you gain peace of mind and control over your healthcare choices.

Read More:

- Affordable Health Insurance Quotes: Save Money on Quality Coverage

- Short Term Health Insurance Online: Fast, Flexible Coverage Today

- Compare Family Health Insurance Plans: Find the Best Coverage

- Best Private Health Insurance Plans: Top Choices for 2024

- Medicare Supplement Plans Comparison: Find the Best Coverage

- Medicare Prescription Drug Plans: Save More on Your Medications

- Medicare Dental and Vision Coverage: What You Need to Know

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage